My wife certainly will not mind that I broadcast the fact that she is an excellent cook; however, I may catch some flak for letting you know that she is also a picky eater. This makes for an interesting dichotomy in our kitchen. On the one hand, she pushes herself to experiment in making new dishes; on the other hand, she refuses to try many of them. That’s right — my wife is a cook who occasionally will not eat her own cooking.

That leaves yours truly to be the official taste tester of the dishes she will not try herself. Fortunately for me, her flavors are usually on point, and I trust her not to poison me. But I also kid that it would be an awkward situation if I were a customer in her restaurant, as I am not sure anyone would want to touch a plate that the chef herself would not eat.

Fund Managers Who Eat Their Own Cooking Tend to Outperform

Thanks to some new research on mutual fund performance, it is clear that it is not only diners who should insist that those in charge eat their own cooking. Investors should as well.

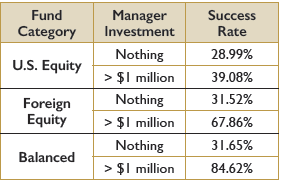

In his recent study entitled “Why You Should Invest with Managers Who Eat Their Own Cooking,” Morningstar analyst Russel Kinnel looked at mutual fund manager investment levels in their own funds as of 2009. He then looked at the performance of these actively-managed funds over the next five years. He then measured each fund’s success rate, which he defined as funds that outperformed their investment category. The results are interesting, although not all that surprising:

The results are not that surprising because one would expect a fund manager with a significant amount of his or her personal money in the fund to do better than one with no investment at all. It is an extra incentive beyond keeping your job and getting paid more.

The other interesting finding from the Morningstar study was that this relation-ship did not hold with taxable bond funds. Fixed income managers with no money invested in their fund were no more or less likely to outperform their investment category than those managers with over one million dollars invested. Yet despite that fact, the widest disparity in success rates between uninvested managers and heavily-invested managers was found in the balanced fund category, where bonds are part of the allocation.

Additional Research

American Funds found a similar link between manager ownership and fund performance in a recently-released study. Their study is a bit broader in scope in terms of time as they looked at 20 years’ worth of fund returns (1994-2013), but they only covered two investment categories — actively-managed U.S. and foreign largecap equity funds.

The results of their study are strikingly similar to those of Morningstar’s study. U.S. equity funds with the highest ownership — defined as having at least one portfolio manager with at least $1 million invested in the fund — outperformed the S&P 500 Index in 70% of rolling ten-year periods (based on monthly data). This compares to just 27% of all U.S. equity funds. For foreign funds, 58% of the high-ownership group outperformed the MSCI All Country World ex-USA Index compared to just 31% of all foreign equity funds.

Investor Implications

Although this research is new, it provides evidence that equity investors can benefit by investing with managers who have a significant amount of their own money invested in their funds. Management investment levels can be found in the fund’s Statement of Additional Information, which can be obtained on the fund company’s website.

And while registered investment advisors are not required by the SEC to publicly disclose their personal investments like mutual fund managers are, we are proud to state that Bell eats its own cooking.